Table Of Content

And with current mortgage rates doubling in 2022, it has been a top factor in slowing down home purchases heading into 2023. Even a few basis points can make the difference between a home being affordable or out of reach (a basis point equals one-hundredth of a percentage point). So don’t feel like you’re stuck with the rate of the first lender you meet.

How can I start my mortgage application?

On the House: How Much House Can You Really Afford? - Realtor.com News

On the House: How Much House Can You Really Afford?.

Posted: Tue, 11 Jul 2023 07:00:00 GMT [source]

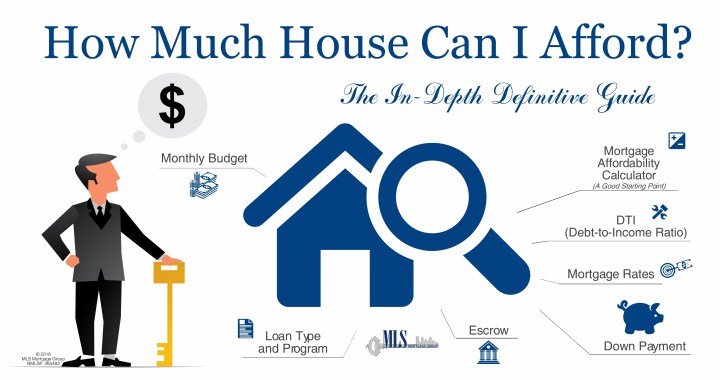

Let’s say your car payment, credit card payment and student loan payment add up to $1,050 per month. Your proposed housing payment, then, could be somewhere between 26% and 35% of your income, or $1,820 to $2,450. Remember, your monthly house payment includes more than just repaying the amount you borrowed to purchase the home. The "principal" is the amount you borrowed and have to pay back (the loan itself), and the interest is the amount the lender charges for lending you the money. Depending upon your property location, property type, and loan amount, you may have other monthly or annual expenses such as mortgage insurance, flood insurance, or homeowner association fees. Please visit our VA Mortgage Calculator to get more in-depth information regarding VA loans, or to calculate estimated monthly payments on VA mortgages.

Home affordability begins with your mortgage rate

The type of mortgage loan you choose to apply for can affect how much house you’re able to afford. As such, it’s important to have a clear sense of what each loan option will entail as you begin your home-buying journey. You might think you need to plunk down 20% of your purchase price for a down payment, but that’s actually not true. You can get a conventional loan (a loan not backed by a government agency) for as little as 3% down. Suppose you bought the same $200,000 house as above with the 15-year fixed mortgage at 5% but the mortgage interest rate changed to 6.25%. You will have an easier time making your payments, or (better yet!) you will be able to pay extra on the principal and save yourself money by paying off your mortgage early.

How does your debt-to-income ratio impact affordability?

And they don’t know if you’re saving enough for retirement or if you send half your paycheck to your parents every month. If you have a VA loan, guaranteed by the Department of Veterans Affairs, you won’t have to put anything down or pay for mortgage insurance, but you will have to pay a funding fee. Fees depend on how many amenities the community has, how many services it requires, and how much upkeep it needs. Local real estate listings can give you an idea about the homeowners association fees in the neighborhoods, condos or townhomes you’re interested in. Some homes are in a special flood hazard area; this means you’ll probably be required to buy flood insurance. Other homes are in locations where lenders will not require you to buy flood insurance.

Once again, the answer to this question will depend on where you want to buy and what kind of property you want. Your credit score and DTI will also be important factors in determining what interest rate and loan terms you get from the lender. The rule of thumb is to meet with at least three lenders to compare mortgage rates but five is often preferred. The more quotes you get, the greater possibility that you can save thousands of dollars over the life of your loan.

Find Affordable Mortgage Options

Average annual premiums usually cost less than 1% of the home price and protect your liability as the property owner and insure against hazards, loss, etc. Private Mortgage Insurance (PMI) is calculated based on your credit score and amount of down payment. If your loan amount is greater than 80% of the home purchase price, lenders require insurance on their investment. The back-end debt ratio includes everything in the front-end ratio dealing with housing costs, along with any accrued recurring monthly debt like car loans, student loans, and credit cards.

Find the right loan for the home you love

You can also check out current mortgage rates in your area for an idea of what the market looks like. Lenders generally want to know you will have a cash reserve remaining after you’ve purchased your home and moved in, so you don’t want to empty your savings account on a down payment. They don’t know how much you spend on groceries, child care, entertainment or travel. They don’t know if you’re planning to quit your job and start a business that might make your income irregular.

What can you afford to spend on a house? Try our SoCal-specific calculator.

New residents should know that the cost of living in Los Angeles is higher than in many other parts of the United States, particularly when it comes to housing. Researching neighborhoods and planning for commuting times can help in making a successful transition. Additionally, embracing the diverse culture and exploring different parts of the city can lead to discovering hidden gems and building a connection to the community. Claiming the seventh spot on our list of affordable Los Angeles suburbs is Downey.

Or instead of entering a dollar amount, enter the down payment percentage in the window to the right. A down payment is the cash you pay upfront for a home, and home equity is the value of the home, minus what you owe. Conforming loans have maximum loan amounts that are set by the government and conform to other rules set by Fannie Mae or Freddie Mac, the companies that provide backing for conforming loans.

This video shows you how your mortgage payment should fit comfortably into your lifestyle. Most states have first-time home buyer assistance programs designed to make homeownership more affordable. The exact amount you’ll qualify for will depend on your finances and vary from lender to lender. The best way to determine how much mortgage you can qualify for is to start the mortgage application process. Look at your full financial picture after you’ve tracked your income and expenses for a few months. For example, if you realize you have $3,000 left over at the end of each month, decide how much of that could be allocated toward a mortgage.

Conventional loans can come with down payments as low as 3%, although qualifying is a bit tougher than with FHA loans. Monterey Park takes the final spot on our list of affordable Los Angeles suburbs you’ll want to consider moving to. Without traffic, you’ll find yourself in Los Angeles in roughly 15 minutes.

If your loan requires other types of insurance like private mortgage insurance (PMI) or homeowner's association dues (HOA), these premiums may also be included in your total mortgage payment. Most financial advisors agree that people should spend no more than 28 percent of their gross monthly income on housing expenses, and no more than 36 percent on total debt. The 28/36 percent rule is a tried-and-true home affordability rule of thumb that establishes a baseline for what you can afford to pay every month. That means your mortgage payment should be a maximum of $1,120 (28 percent of $4,000), and your other debts should add up to no more than $1,440 each month (36 percent of $4,000). You’ll need to determine a budget that allows you to pay for essentials like food and transportation, wants like entertainment and dining out, and savings goals like retirement. And don’t forget you’d also need to pay a down payment and closing costs upfront, while keeping enough leftover to cover regular maintenance, upkeep and any emergency repairs that may arise.

Explore mortgage options to fit your purchasing scenario and save money. The exact amount you should spend on a new home depends on your financial situation. Ideally, you’ll want to avoid spending more than a third of your gross monthly income on your mortgage. However, depending on your finances, you may be able to afford a slightly more expensive home. According to the 29/41 rule, you should spend no more than 29% of your gross income on housing and no more than 41% of your gross income on the sum of all debt payments, housing included. We’ll see what that looks like in a moment, but let’s first discuss how to calculate your DTI.

Once you close on your home loan, your monthly mortgage payment may well be the biggest debt payment you make each month, so it’s important to make sure you can afford it. Your monthly payment and down payment are probably the two biggest factors in determining how much you can afford. The mortgage payments assume a 20% down payment, and they include property taxes and home insurance. Most home loans require at least 3% of the price of the home as a down payment. Although it's a myth that a 20% down payment is required to obtain a loan, keep in mind that the higher your down payment, the lower your monthly payment. A 20% down payment also allows you to avoid paying private mortgage insurance on your loan.

We'll help you estimate how much you can afford to spend on a home. We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money. Bankrate follows a stricteditorial policy, so you can trust that our content is honest and accurate. Our award-winning editors and reporters create honest and accurate content to help you make the right financial decisions. The content created by our editorial staff is objective, factual, and not influenced by our advertisers.

No comments:

Post a Comment